Privacy Policy for economicsmajorsalary.blogspot.com

If you require any more information or have any questions about our privacy policy, please feel free to contact us by email at frqblogger@gmail.com.

At economicsmajorsalary.blogspot.com, the privacy of our visitors is of extreme importance to us. This privacy policy document outlines the types of personal information is received and collected by economicsmajorsalary.blogspot.com and how it is used.

Log Files

Like many other Web sites, economicsmajorsalary.blogspot.com makes use of log files. The information inside the log files includes internet protocol ( IP ) addresses, type of browser, Internet Service Provider ( ISP ), date/time stamp, referring/exit pages, and number of clicks to analyze trends, administer the site, track user’s movement around the site, and gather demographic information. IP addresses, and other such information are not linked to any information that is personally identifiable.

Cookies and Web Beacons

economicsmajorsalary.blogspot.com does use cookies to store information about visitors preferences, record user-specific information on which pages the user access or visit, customize Web page content based on visitors browser type or other information that the visitor sends via their browser.

DoubleClick DART Cookie

.:: Google, as a third party vendor, uses cookies to serve ads on economicsmajorsalary.blogspot.com.

.:: Google's use of the DART cookie enables it to serve ads to users based on their visit to economicsmajorsalary.blogspot.com and other sites on the Internet.

.:: Users may opt out of the use of the DART cookie by visiting the Google ad and content network privacy policy at the following URL - http://www.google.com/privacy_ads.html

Some of our advertising partners may use cookies and web beacons on our site. Our advertising partners include ....

Google Adsense

Amazon

These third-party ad servers or ad networks use technology to the advertisements and links that appear on economicsmajorsalary.blogspot.com send directly to your browsers. They automatically receive your IP address when this occurs. Other technologies ( such as cookies, JavaScript, or Web Beacons ) may also be used by the third-party ad networks to measure the effectiveness of their advertisements and / or to personalize the advertising content that you see.

economicsmajorsalary.blogspot.com has no access to or control over these cookies that are used by third-party advertisers.

You should consult the respective privacy policies of these third-party ad servers for more detailed information on their practices as well as for instructions about how to opt-out of certain practices. economicsmajorsalary.blogspot.com's privacy policy does not apply to, and we cannot control the activities of, such other advertisers or web sites.

If you wish to disable cookies, you may do so through your individual browser options. More detailed information about cookie management with specific web browsers can be found at the browsers' respective websites.

Thursday, March 24, 2011

The Business Economics Major

If you wish you had known more before this economic recession hit and you find yourself brainstorming ways out of this mess, then perhaps pursing a Business Economics major is for you! At an economics college, you'll learn about many aspects of business, management, finance, marketing and corporate planning, in addition to the money management issues of today. The majority of people working in applied economics hold positions as forecasters, analysts, market researchers, government workers and client support personnel.

As you may have heard, the choice of school and the pursuit of a degree are extremely important in determining your success in economics. Just about every school offers macro economics and microeconomics courses, but to really get ahead, you'll want to get into a graduate school with the best department of Economics you can find. The best schools may offer more passionate teachers, better internship options, more extensive areas of study and the sort of prestige you'll need when looking to start your career in the competitive labor market.

When choosing classes from a school's department of Economics, the best advice is to take more math courses! It can be easy to fall behind in your studies if you aren't crystal clear on the statistics, calculus and mathematical concepts. When you were trying to get your bachelor's degree in economics, you were likely scanning the course options for "easy electives" and ways of pulling your GPA up. However, graduate schools care most about what hard classes you've taken and how well you did in them, rather than your GPA as a whole. Be sure you take real analysis, calculus and econometrics, as these classes will be vital to your understanding.

To get an undergrad degree in Business Economics, students attending an accredited economics university will need to take courses like macro economics, microeconomics, financial accounting and reporting, calculus, economics statistics, econometrics, money/banking/credit, business writing, the stock market, labor economics, monetary economics, international trade theory, law and economics, industrial organization, economics and business strategy, organizational psychology, formal organizations and politics and the economy.

The average starting salary for economists is $38,000 for a bachelor's degree, $48,000 for a master's and $70,000 for a PhD, according to a 2002 National Association of Business Economics survey. The median income for the economics major is higher than any other major, experts say. Economics research also suggests that economics majors earn 20% more than business administration majors, 19% more than accounting majors, 18% more than marketing majors and 15% more than finance majors. When a potential employer sees this major on a resume, he or she immediately understands that you have a solid foundation of math, politics, business and economic theory. Your degree also shows that you have the capacity to process complex subjects and problem solve, which is valuable in any field.

According to US News & World Report, Harvard University in Boston, Massachusetts is the top-rated school for Business Economics. The second-best university in this field is Stanford in California and Northwestern University in Illinois. After the top-three, other economics college options include the University of Pennsylvania (Wharton) in Philadelphia, the Massachusetts Institute of Technology (Sloan) in Cambridge, the University of Chicago, UC-Berkeley in California, Dartmouth College in New Hampshire, Columbia University in New York City and Yale University in Connecticut. It's highly recommended that individuals looking to remain competitive in their field pursue advanced education with Master's or PhD's.

Unlike undergrad, the department of Economics in grad schools looks to cultivate the best and brightest talent. Most students are granted a fellowship, assistantship, grant, tuition remission or monthly stipend to cover the cost of the program and living expenses. Be aware that you'll be required to do a lot of dirty work for your money, like grading, teaching, lecturing, leading weekly section meetings, researching and writing. If a lot of students are admitted, then you may still need to pay or seek NSF grants on your own. The good news is that, after all their hard work, 99% of graduate students get placed into applied economics positions right out of grad school.

As you may have heard, the choice of school and the pursuit of a degree are extremely important in determining your success in economics. Just about every school offers macro economics and microeconomics courses, but to really get ahead, you'll want to get into a graduate school with the best department of Economics you can find. The best schools may offer more passionate teachers, better internship options, more extensive areas of study and the sort of prestige you'll need when looking to start your career in the competitive labor market.

When choosing classes from a school's department of Economics, the best advice is to take more math courses! It can be easy to fall behind in your studies if you aren't crystal clear on the statistics, calculus and mathematical concepts. When you were trying to get your bachelor's degree in economics, you were likely scanning the course options for "easy electives" and ways of pulling your GPA up. However, graduate schools care most about what hard classes you've taken and how well you did in them, rather than your GPA as a whole. Be sure you take real analysis, calculus and econometrics, as these classes will be vital to your understanding.

To get an undergrad degree in Business Economics, students attending an accredited economics university will need to take courses like macro economics, microeconomics, financial accounting and reporting, calculus, economics statistics, econometrics, money/banking/credit, business writing, the stock market, labor economics, monetary economics, international trade theory, law and economics, industrial organization, economics and business strategy, organizational psychology, formal organizations and politics and the economy.

The average starting salary for economists is $38,000 for a bachelor's degree, $48,000 for a master's and $70,000 for a PhD, according to a 2002 National Association of Business Economics survey. The median income for the economics major is higher than any other major, experts say. Economics research also suggests that economics majors earn 20% more than business administration majors, 19% more than accounting majors, 18% more than marketing majors and 15% more than finance majors. When a potential employer sees this major on a resume, he or she immediately understands that you have a solid foundation of math, politics, business and economic theory. Your degree also shows that you have the capacity to process complex subjects and problem solve, which is valuable in any field.

According to US News & World Report, Harvard University in Boston, Massachusetts is the top-rated school for Business Economics. The second-best university in this field is Stanford in California and Northwestern University in Illinois. After the top-three, other economics college options include the University of Pennsylvania (Wharton) in Philadelphia, the Massachusetts Institute of Technology (Sloan) in Cambridge, the University of Chicago, UC-Berkeley in California, Dartmouth College in New Hampshire, Columbia University in New York City and Yale University in Connecticut. It's highly recommended that individuals looking to remain competitive in their field pursue advanced education with Master's or PhD's.

Unlike undergrad, the department of Economics in grad schools looks to cultivate the best and brightest talent. Most students are granted a fellowship, assistantship, grant, tuition remission or monthly stipend to cover the cost of the program and living expenses. Be aware that you'll be required to do a lot of dirty work for your money, like grading, teaching, lecturing, leading weekly section meetings, researching and writing. If a lot of students are admitted, then you may still need to pay or seek NSF grants on your own. The good news is that, after all their hard work, 99% of graduate students get placed into applied economics positions right out of grad school.

How to Earn Impressive Actuarial Salary?

Nature of Work

As mentioned above, an actuary's primary responsibility is to create strategies that can capacitate any financial business with strength and insight to counter uncertainties and unfavorable impacts. Actuaries are mostly found in the field of insurance where they calculate the effects of major incidents like natural disasters, accidents and deaths. Through such assessment, actuaries help minimize the impact of losses on their clients' finances. Collection of pertinent data and study of the same are major parts of an actuary's professional duties.

Educational Qualification

To become an actuary, you could take up an advanced degree in actuarial science. You can also achieve competency in this field of study by taking up online education. An actuarial science degree consists of subjects like calculus, statistics, business communication, finance and economics. Apart from an actuarial science degree, a degree in economics, math, finance or even business can make you an actuary. Though the actuarial science degree is the most preferred, you can successfully get a job only when you clear the actuarial exams.

Compensation

Actuarial jobs are considered niche all over the world. In the United Kingdom, there are only about 9000 registered actuaries presently. While very few students prepare to be actuaries, the demand for them is quite high. For the very same reason, actuaries are paid high salaries. Actuarial salary in the United States can range from anywhere between $55, 000 and $115, 000. The pay of a student holding an actuarial science degree can start anywhere between $50, 000 and $54, 000.

Actuarial salary being higher than packages paid in most other jobs, are decided on the basis of a few factors like the duration of professional experience, actuary examination passed and the knowledge of computers.

The best actuarial jobs are out there. With the right education, you too can get impressive actuarial salary. Visit the State University website to read Michael Russell talk about all the recent information on online degrees related to actuarial science and associated careers.

As mentioned above, an actuary's primary responsibility is to create strategies that can capacitate any financial business with strength and insight to counter uncertainties and unfavorable impacts. Actuaries are mostly found in the field of insurance where they calculate the effects of major incidents like natural disasters, accidents and deaths. Through such assessment, actuaries help minimize the impact of losses on their clients' finances. Collection of pertinent data and study of the same are major parts of an actuary's professional duties.

Educational Qualification

To become an actuary, you could take up an advanced degree in actuarial science. You can also achieve competency in this field of study by taking up online education. An actuarial science degree consists of subjects like calculus, statistics, business communication, finance and economics. Apart from an actuarial science degree, a degree in economics, math, finance or even business can make you an actuary. Though the actuarial science degree is the most preferred, you can successfully get a job only when you clear the actuarial exams.

Compensation

Actuarial jobs are considered niche all over the world. In the United Kingdom, there are only about 9000 registered actuaries presently. While very few students prepare to be actuaries, the demand for them is quite high. For the very same reason, actuaries are paid high salaries. Actuarial salary in the United States can range from anywhere between $55, 000 and $115, 000. The pay of a student holding an actuarial science degree can start anywhere between $50, 000 and $54, 000.

Actuarial salary being higher than packages paid in most other jobs, are decided on the basis of a few factors like the duration of professional experience, actuary examination passed and the knowledge of computers.

The best actuarial jobs are out there. With the right education, you too can get impressive actuarial salary. Visit the State University website to read Michael Russell talk about all the recent information on online degrees related to actuarial science and associated careers.

Thursday, August 19, 2010

International Growth Highlights Wal-Mart's 2Q

We own WalMart (WMT) because it adopted value-based management a few years back. It made return on invested capital its overarching objective. The result was a change in strategy. Instead of driving sales growth by investing vast amounts in new stores in already saturated markets, WMT cut back on domestic capital spending and drove US productivity.

It also exited markets like Germany where expected returns were below its cost of capital. The growth would come from the fast growing emerging markets of China and South America. Those are the places that very profitable growth continues as was reported in today's earnings release. From Morningstar $$:

Wal-Mart's competitive advantages and everyday low pricing strategy will stand under any operating environment. Moreover, as Wal-Mart gains traction in several high-growth markets such as Mexico, China, and Brazil, the international segment will become an increasingly critical component of our valuation assumptions. Trading at less than 13 times our forward earnings estimate and an enterprise value/EBITDA under 7 times, Wal-Mart shares look attractive.

Using excess cash flow to reduce shares outstanding has added about 2% to EPS growth since 2005. With recession over in its business, WMT has stepped up buying shares so the increased ownership for existing shareholders will add about 4% to EPS growth.

Intrinsic Value

In the graph below we see WalMart's intrinsic value (red line) as measured by afgview.com's default model matched up against share price (the blue columns). You can see the increasing gap between a rising intrinsic value and falling or at best stagnant stock price. These are widening gaps give us our margin of safety. We can see that after the recession '08-09, the gap is beginning to widen again.

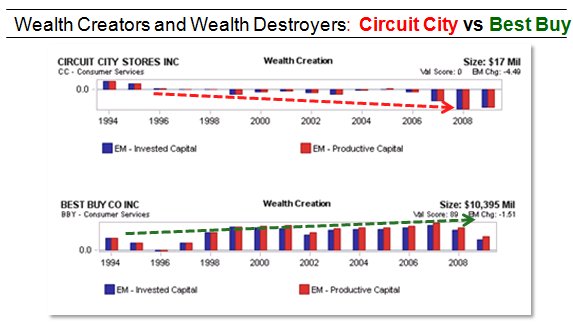

Wealth Creators vs. Wealth Destroyers: Best Buy Co., Inc. (NYSE:BBY) vs. Circuit City

Analysts tend to miss the forest for the trees. In retail they are obsessed with the business model drivers like sales per square foot, same store sales or gross margin. Certainly, these metrics are important for understanding the dynamics of a retail business - but to what end?

The bottom line is whether a business model and management team create value per share - that's the single minded objective function for any for profit business. It's the only one that allows for principled trade-offs between competing subordinate goals. The answer is always the combination of drivers that will yield the most value over time.

AFGview.com's economic margin framework accomplishes this simple but overlooked goal. See below for an example comparison of Best Buy to Circuit City.

On ValueExpectations.com we always talk about a company’s true economic profitability (Economic Margin) to see through some of the distortions caused by traditional accounting practices and better understand what a company is truly earning above or below its cost of capital# We have shown through numerous examples that a company’s Economic Margin (EM) level is highly correlated with its market performance and an increase in margins typically leads to market out performance, where a decline in margins leads to market under performance# The example below shows both ends of the spectrum, one company that generates positive EMs and is able to grow its business while maintaining its profitability while the other company was unable to earn its cost of capital and consistently deteriorated its EMs.

It is no surprise based on economic profitability that Best Buy Co., Inc. is still doing quite well in the retail arena and has done a good job of growing its business while maintaining its profitability. The market tends to reward companies that grow profitable businesses and relative to the market BBY has consistently outperformed the S&P 500. Circuit City on the other hand deteriorated its EMs over time and eventually was unable to survive.

The Economic Margin (EM) Framework was developed to evaluate corporate performance from an economic cash flow perspective and is an alternative to accounting-based valuation metrics. EM measures the return a company earns above or below its cost of capital and provides a more complete view of a company’s underlying economic strength.

EM is meant to serves two purposes: Create a measure of a company’s economic profitability; that is, did this company generate cash flow in excess of the costs of its capital invested in its operations, or did the company destroy wealth? Once we have solved for this, we can then use this EM as a function in our valuation model.

EM is calculated by dividing a company’s Operating Cash Flow minus Capital Charge by their Invested Capital.

It is not uncommon for companies to grow EPS while having declining or negative EM’s. This occurs when the cost for the investment required to yield the EPS (cost of capital) is more than the cash flow generated from the investment. From an economic perspective, this is growing EPS at the expense of the economics of the business.

Unlike traditional measures, EM considers the “profitability” of EPS growth, eliminates accounting distortions, and are comparable across time and industry. By analyzing a company’s EMs through time, investors gain a more accurate account of levels and changes in a company’s current profitability and value.

Structure and Development of the Economy

With its strategic location at the doorway to the Mainland and on the international time zone that bridges the time gap between Asia and Europe, the HKSAR has been serving as a global centre for trade, finance, business and communications. Hong Kong is now ranked the 11th largest trading entity in the world. It operates the busiest container port in the world in terms of throughput, as well as one of the busiest airports in terms of number of international passengers and volume of international cargo handled. In addition, it is the world's 12th largest banking centre in terms of external banking transactions, and the seventh largest foreign exchange market in terms of turnover. Its stock market is Asia's second largest in terms of market capitalisation.

Hong Kong is characterised by a high degree of internationalisation, business-friendly environment, rule of law, free trade and free flow of information, open and fair competition, well-established and comprehensive financial network, superb transport and communications infrastructure, sophisticated support services, and a skilled and well educated workforce complemented by a pool of effective and enterprising entrepreneurs. Added to these are the substantial amount of fiscal reserves and foreign exchange reserves, a fully convertible and stable currency, and a simple tax system with a low tax rate. On these virtues, Hong Kong is widely regarded as amongst the freest and most competitive economies in the world. The US Heritage Foundation ranks Hong Kong as the world's freest economy for the 10th year in a row in 2004. The Cato Institute of the United States, in conjunction with the Fraser Institute of Canada and other research bodies around the world, also consistently ranks Hong Kong as the freest economy in the world.

Over the past two decades, the Hong Kong economy has more than doubled in size, with GDP growing at an average annual rate of 5.0 per cent in real terms. This outpaces considerably the growth of the world economy and the Organisation for Economic Cooperation and Development (OECD) economies. Over the same period, Hong Kong's per capita GDP doubled at constant price level, giving an average annual growth rate of 3.7 per cent in real terms. At US$23,300 in 2003, this per capita GDP was amongst the highest in Asia, next only to Japan (Chart 1).

In line with increased external orientation of the Hong Kong economy, trade in goods expanded by eight times and trade in services by almost three times in real terms over the past two decades. In 2003, the total value of visible trade (comprising re-exports, domestic exports and imports of goods) reached $3,543 billion, corresponding to 287 per cent of GDP. This was distinctly larger than the ratios of 156 per cent in 1983 and 230 per cent in 1993. If the value of exports and imports of services is also taken into account, the ratio is even greater, at 331 per cent in 2003, as compared to 192 per cent in 1983 and 267 per cent in 1993.

Chart 1

Gross Domestic Product

(year-on-year rate of change in real terms)

Over the past two decades, the Hong Kong economy grew at an average annual rate of 5.0 per cent in real terms, outpacing the corresponding growth rate of 2.8 per cent for OECD economies as a whole. In 2003, the economy still attained a 3.3 per cent growth in real terms, despite the impact of SARS.

As another indication of the high degree of external orientation, the stock of inward direct investment in Hong Kong amounted to $2,622 billion in market value at end-2002, equivalent to 208 per cent of GDP. Hong Kong is the second most favoured destination for inward direct investment in Asia, next only to the Mainland. The corresponding figures for the stock of outward direct investment in Hong Kong were likewise substantial, at $2,413 billion and 192 per cent of GDP, much larger than those for many other economies in Asia. As a major financial centre in the region with huge cross-territory fund flows, Hong Kong's external financial assets and liabilities were also substantial, at $8,033 billion and $5,355 billion respectively at end-2002. The corresponding ratios to GDP in that year were 638 per cent and 425 per cent. Reflecting Hong Kong's sound international investment position, net external financial assets amounted to $2,677 billion at end-2002, equivalent to 213 per cent of GDP. As to gross external debt, which is the sum of the non-equity liability components in international investment, it stood at $2,803 billion at end-2003, equivalent to 227 per cent of GDP. Yet a major proportion of it arose from normal operations of the banking sector, and the Government incurred no external debt at all.

The Gross National Product (GNP), comprising GDP and net external factor income flows, stood at $1,269 billion in 2003. This was higher than the corresponding GDP by 2.8 per cent, owing to sustained net inflow of external factor income. In gross terms, inflows and outflows of external factor income remained substantial in 2003, at $329 billion and $294 billion respectively, equivalent to 27 per cent and 24 per cent of GDP. This was related to the huge volume of both inward and outward investment in Hong Kong.

Contributions of the Various Economic Sectors

Primary production (including agriculture, fisheries, mining and quarrying) is insignificant in Hong Kong, in terms of both value added contribution to GDP and share in total employment. This reflects the predominantly urbanised nature of the economy.

Secondary production (comprising manufacturing, construction, and supply of electricity, gas and water), which constituted a significant contributor to GDP up to the early 1980s, has diminished in relative importance since then. Within this broad sector, the value added contribution from manufacturing shrank from 21 per cent in 1982 to 14 per cent in 1992 and distinctly more to only 5 per cent in 2002, consequential to ongoing relocation of the more labour-intensive production processes to the Mainland. For the construction sector, its contribution to GDP edged lower from 7 per cent in 1982 to 5 per cent in 1992, and further to 4 per cent in 2002. As to supply of electricity, gas and water, the corresponding share held relatively stable, at around 2-3 per cent over the past two decades.

The open door policy and economic reform in the Mainland have not only provided an enormous production hinterland and market outlet for Hong Kong's manufacturers, but have also created abundant business opportunities for a wide range of service activities. These activities include specifically freight and passenger transport, travel and tourism, telecommunications, banking, insurance, real estate, and professional services such as financial, legal, accounting and consultancy services. In consequence, the Hong Kong economy has become increasingly service-oriented since the 1980s.

Reflecting this, the share of the tertiary services sector (comprising the wholesale, retail and import/export trades, restaurants and hotels; transport, storage and communications; financing, insurance, real estate and business services; community, social and personal services; and ownership of premises) in GDP went up visibly, from 69 per cent in 1982 to 79 per cent in 1992 and further to 88 per cent in 2002 (Chart 2).

The profound change in the economic structure was also borne out by a broadly similar shift in the sectoral composition of employment. Over the past two decades, the share of the services sector in total employment followed a continuous uptrend, rising distinctly from 52 per cent in 1983 to 73 per cent in 1993 and further to 85 per cent in the first three quarters of 2003. On the other hand, the corresponding share for the manufacturing sector kept on shrinking, from 38 per cent in 1983 to 18 per cent in 1993 and further to only 5 per cent in the first three quarters of 2003 (Chart 3).

The services sector has not only flourished but also diversified in types of activities, concomitant with the structural transformation of the economy. Trade-related and tourism-related services, community, social and personal services, and finance and business services such as banking, insurance, real estate and a host of related professional services, have all grown distinctly over the past two decades. Strong expansion was also observed in information technology in the more recent years, especially those pertaining to telecommunications services and Internet applications, in line with the shift in economic structure more towards knowledge-based activities.

Chart 2

Gross Domestic Product by broad economic sector

Along with a profound shift in economic structure, the share of the tertiary services sector in GDP continued to increase, while the share of the secondary sector dwindled further over the past two decades.

Chart 3

Employment by broad economic sector

Consequential to the ongoing relocation of the less skill-intensive and lower value added manufacturing processes to the Mainland, as well as the strong growth in service activities in Hong Kong, the tertiary services sector has expanded markedly and has overtaken the secondary sector to become the largest employer in the economy since 1981.

* Average of Q1 to Q3 2003.

On trade in services, exports and imports of services both grew by an annual average of 7 per cent in real terms over the past two decades. In 2002, civil aviation, travel and tourism, trade-related services, and various financial and banking services were the largest components of trade in services. Within exports of services, offshore trading and merchandising services have overtaken transportation as the most important component in 2002, accounting for 35 per cent of the total value in that year. For transportation, the corresponding share was 30 per cent. This was followed by travel and tourism (with a share of 17 per cent), and financial and banking services (6 per cent). As to imports of services, travel and tourism remained the largest component, accounting for 50 per cent of the total value in 2002. Transportation was in the second place (with a share of 26 per cent), followed by offshore trading and merchandising services (7 per cent), and financial and banking services (3 per cent).

Net output or value added of the services sector as a whole rose visibly, by an annual average of 6 per cent in value terms between 1992 and 2002. Amongst the major constituent sectors, net output of community, social and personal services had the fastest growth (at an average annual rate of 9 per cent). This was followed by transport, storage and communications (6 per cent); the wholesale, retail and import/export trades, restaurants and hotels (5 per cent); and financing, insurance, real estate and business services (4 per cent).

In terms of value added contribution to GDP, the wholesale, retail and import/export trades, restaurants and hotels continued to be the largest in 2002, with a share of 27 per cent. This was followed by community, social and personal services (22 per cent), financing, insurance, real estate and business services (22 per cent), and transport, storage and communications (11 per cent) (Chart 4).

Chart 4

Gross Domestic Product by major service sector

Over the past two decades, community, social and personal services had a more distinct increase in net output than other major service sectors. Yet ranked in terms of value added contribution to GDP, the wholesale, retail and import/export trades, restaurants and hotels remained the largest service sector in 2002.

In terms of employment, the wholesale, retail and import/export trades, restaurants and hotels was again the largest sector, accounting for 31 per cent of the total employment in the first three quarters of 2003. This was followed by community, social and personal services (with a share of 28 per cent), financing, insurance, real estate and business services (15 per cent), and transport, storage and communications (11 per cent) (Chart 5).

Chart 5

Employment by major service sector

Over the past two decades, financing, insurance, real estate and business services showed the fastest employment growth. But in terms of employment size, the wholesale, retail and import/export trades, restaurants and hotels continued to be the largest employer in the economy in 2003. * Average of Q1 to Q3 2003. The Manufacturing Sector Manufacturing firms in Hong Kong are renowned for their versatility and flexibility in coping with changing demand conditions in the overseas markets. Moreover, through increased outward processing arrangements in the Mainland, Hong Kong's productive capacity has effectively been expanded by multiples, which has helped uphold the price competitiveness of its products. Besides relocating the more labour-intensive production processes to the Mainland, Hong Kong's manufacturers have also been striving hard to diversify their products and markets, in face of the challenges from globalisation of trade and keen competition from other export producers. Concurrently, productive efficiency and product quality have been continuously upgraded by incorporating more advanced skills and technology. Within the local manufacturing sector, textiles and clothing remain the most important industries, notwithstanding continued decline in their relative significance over the years. Other major industries include machinery and equipment, electronics, printing and publishing, food processing and metal products. Generally speaking, those manufacturing operations still remaining in Hong Kong are more knowledge-based with a higher value added and a greater technology content. Between 1993 and 2003, labour productivity in the local manufacturing sector, as measured by the ratio of the industrial production index to the manufacturing employment index, rose visibly, by an annual average of around 6 per cent. In 2003, the United States and the Mainland were the two largest markets for Hong Kong's domestic exports, accounting for 32 per cent and 30 per cent respectively of the total. Other major markets included the United Kingdom (6 per cent), Germany (4 per cent), Taiwan (3 per cent), Japan (2 per cent), and the Netherlands (2 per cent). In the more recent years, new markets have been developed for Hong Kong's exports, including markets in the Middle East, Eastern Europe, Latin America and Africa. Increasing Economic Links between the HKSAR and the Mainland Since the Mainland adopted its economic reform and open door policy in 1978, economic links between Hong Kong and the Mainland have gone from strength to strength. This has brought substantial economic benefits to both places. Visible trade between Hong Kong and the Mainland has expanded rapidly since 1978, at an average annual rate of 22 per cent in value terms. But the pace of growth moderated in the more recent years, to an annual average of 8 per cent during 1993-2003, partly due to increased direct shipment of goods into and out of the Mainland upon enhancement of port facilities and simplification of customs procedures there. The Mainland remained Hong Kong's largest trading partner in 2003, accounting for 43 per cent of the total trade value in Hong Kong. The bulk (specifically, 91 per cent) of Hong Kong's re-export trade was related to the Mainland, making it the largest market for as well as the largest source of Hong Kong's re-exports. Reciprocally, Hong Kong was the Mainland's third largest trading partner in 2003 (after Japan and the United States), accounting for 10 per cent of the Mainland's total trade value (Chart 6). In the more recent years, there has been an increasing shift in the mode of Hong Kong-Mainland trade from re-exports to offshore trade. Between 1990 and 1995, Hong Kong's exports of trade-related services grew at an annual average rate of 5 per cent in real terms, much slower than the growth in re-exports involving the Mainland, at an annual average rate of 22 per cent. The growth pattern was reversed during 1995 to 2003, when exports of trade-related services surged at an average annual rate of 15 per cent in real terms, outpacing the growth in re-exports involving the Mainland, at an average annual rate of 7 per cent. Over the past two decades, there has also been a sharp increase in people, service and investment flows between Hong Kong and the Mainland. Hong Kong is a major service centre for the Mainland generally and South China in particular, providing a wide array of financial and other business support services like banking and finance, insurance, transport, accounting and sales promotion. Hong Kong is also a principal gateway to the Mainland for business and tourism. Between 1993 and 2003, the number of trips made by Hong Kong residents to the Mainland grew at an average annual rate of 9 per cent to 53 million trips, and the number of trips made by foreign visitors to the Mainland through Hong Kong at an average annual rate of 4 per cent to 2.7 million trips. Yet, mainly due to the outbreak of SARS in the region in the first half of the year, these two particular types of trips decreased by 6 per cent and 21 per cent respectively in 2003. Chart 6 Visible trade between Hong Kong and the Mainland

|

Economic Value Added (EVA) - How to Calculate Economic Viability of a Corporation

i) Economic Value Added is used as a performance evaluation tool of higher level managers, directors, VPs and CEOs of a corporation because the performance of the organization depends on the human resources deployed.

ii) Economic Value Added is used at sub-division level & entire organizational level of the business, unlike other methods such as Market Value Added that only focuses on the big picture of a corporation.

iii) Economic Value Added factors in to performance evaluation that the operating net income of a corporation must cover both operating costs of the organization as well as the capital costs (opportunity cost of capital). This is unlike other accounting methods such as EBIT or EBITDA or Net Income that look at total revenues generated by the business minus total expenses as a performance evaluation tool.

Subscribe to:

Posts (Atom)